|

Uncoated free-sheet mills react to challenging 10% drop in demand

by WILL MIES, Editorial Director, Worldwide News Service

GRADE STRUCTURE. Uncoated free-sheet paper (uncoated woodfree in Canada and Europe) is made from chemical pulp but may contain up to 10% mechanical pulp as well as deinked recycled fiber.

Major end uses for uncoated free-sheet paper include: business papers, including cut-size or reprographic bond (40% of apparent consumption); offset rolls (21%); forms bond (9%); woven envelope (9%); offset sheets (7.4%); carbonless (4.5%); cover and text (2.2%); tablet (1.5%); kraft envelope (1.5%), ; machine-finished and supercalendered (0.4%); and all other (3.5%). Other uses include thin papers, carbonizing, condenser, cigarette paper, and bibles.

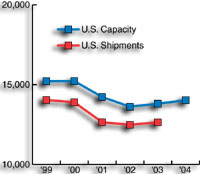

DEMAND/SUPPLY. With last year’s 1.3% decline in demand, the U.S. uncoated free-sheet market will have declined for three consecutive years despite the economic recovery since late 2001. This has resulted in an unprecedented 10% drop in demand since 1999.

The main reason for the disconnect between uncoated free-sheet and the economy has been sharp declines in demand in such end-use market segments as forms bond, carbonless, tablet, cover, and text. However, the main business papers segment only declined 1.0% in 2001 and rose about 2% in 2002. Demand for offset rolls, the second-largest end use, dropped nearly 12% in 2001 but declined less than 1% last year. The decline in many of these end-use markets has been caused by the competitive impact of electronic communication.

Faced with this drop in demand, producers have been working to reduce supply and have kept inventories under tight control. Last year U.S. shipments of uncoated free-sheet dropped 1.3% to 12.5 million tons from the previous year, and mill inventories at the end of 2002 were 7.4% below a year ago. Imports of uncoated free-sheet declined 14.5% to 1.27 million tons, despite a slight rise in imports from Canada. U.S. mills ran at 92% of capacity in 2002, up from 89% the previous year due to significant capacity shutdowns.

CAPACITY. Uncoated free-sheet capacity dropped from a peak of 15.2 million tons in 2000 to 13.6 million tons in 2002, the lowest level in almost a decade. The drop of 1.6 million tons represented more than a 10% decline within a two-year period. Among mills or machines shutting down were International Paper Co. (Lock Haven, Pa., and Erie, Pa.), Nexfor Inc. (West Carrollton, Ohio), SAPPI (Mobile, Ala.), and Georgia-Pacific Corp. (Camas, Wash.). Weyerhaeuser Co. started up a 400,000-tpy paper machine at Kingsport, Tenn. (a project acquired with Willamette Industries in early 2002). But the total net gain over 2002-2003 is around 200,000 due to the shut down of four older paper machines. U.S. uncoated free-sheet capacity is expected to grow about 1.3% in 2003, which includes Missota Paper’s restart of the Brainerd, Minn., mill (105,000 tpy).

OUTLOOK. After a strong fourth quarter, uncoated free-sheet shipments were weak in January and February, and there was modest price erosion on offset rolls and cut-size paper. The price of 20-lb reprographic in February was around $800/ton, while 50-lb offset paper was around $660-$700, both levels basically unchanged from a year ago. The decline in uncoated free-sheet prices has been much less severe than on coated grades due to the producer’s tight control of supply. Price of cut-size has only declined about 7% and offset rolls 10% over the past two years in contrast to a more than 20% decline in coated paper prices.

U.S. uncoated free-sheet shipments are projected to grow about 1.3% in 2003 and more than 3% in 2004, with more growth in the economy and a weaker dollar. Operating rates will remain at around a 92% level in 2003. North American producers will probably try for a price increase later this year to offset rising fiber and energy costs.

Find more tissue news, analysis and statistics in the Grade Centers

|